Weekly Market Pulse - Week ending September 6, 2024

Market developments

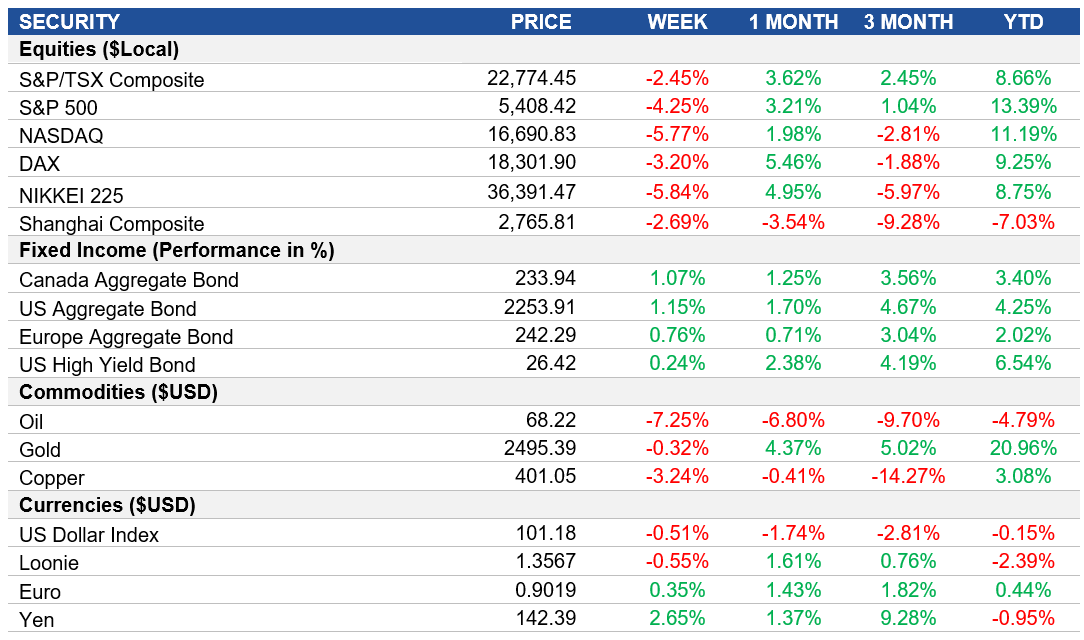

Equities: U.S. stocks suffered their worst week of 2024, led lower by tech and the August jobs report which showed tepid hiring. This fueled concerns about the labour market's health and boosted expectations of a jumbo-sized interest rate cut by the Federal Reserve in September. Additional downward pressure came from a negative earnings release from Broadcom on Friday, along with weaker than expected monthly semiconductor sales data and subpoenas issues by the DOJ to Nvidia earlier this week.

Fixed Income: The world's largest bond market experienced a rally following comments from Federal Reserve Governor Christopher Waller, who indicated that the central bank should initiate interest rate cuts this month. Waller's remarks were a result of disappointing jobs data that suggested a weakening labour market, reinforcing speculation about a significant rate cut at the upcoming Federal Open Market Committee (FOMC) meeting. Canada and Europe also saw yields move lower and bond prices climb higher this week.

Commodities: Despite the support from potential Fed actions, oil prices have erased their gains for 2024 due to fears of a global economic slowdown. In response to these market conditions, OPEC+ announced on Thursday that it would extend voluntary oil production cuts of 2.2 million barrels per day for two additional months, now set to phase out starting December 1, 2024.

Performance (price return)

Source: Bloomberg, as of September 6, 2024

Macro developments

Canada – Softened Contraction in Manufacturing, Bank of Canada Eases Interest Rates Further, Rising Unemployment

The Canadian Manufacturing PMI rose to 49.5 in August, signaling a milder contraction in operating conditions. Weaker declines in output and new orders persisted, while firms faced subdued demand and falling employment. Inflation pressures prompted firms to raise prices, though concerns over costs, interest rates, and delays limited purchasing activity. Business confidence remained positive but cautious.

The Bank of Canada cut its key rate to 4.25% in September, marking its third consecutive cut. The decision aimed to address excess supply in the economy, which was slowing inflation. Despite concerns about undershooting inflation targets, labour market slowdown justified further rate cuts, though inflation remained elevated in some sectors like housing.

Canada’s unemployment rate increased to 6.6% in August, the highest since October 2021. The labour market continued to soften, with more people becoming unemployed, especially among core working-age and older populations. Employment growth was below expectations, while wage growth eased slightly.

U.S. – Manufacturing Stagnation Continues, Job Growth Slows, Unemployment Rate Eases Slightly

The Manufacturing PMI rose slightly to 47.2 in August, marking the 21st month of contraction. New orders and production fell, while employment levels dropped for the third straight month. Despite expectations for disinflation, costs rose at a faster pace, presenting a challenge for the Federal Reserve.

The U.S. added 142K jobs in August, higher than July but below forecasts. Gains were seen in construction, healthcare, and government sectors, while manufacturing employment fell sharply. Overall, job growth aligned with recent trends but lagged the average gains of the past year.

Unemployment rate eased to 4.2% in August, consistent with expectations. The number of unemployed individuals remained steady, while temporary layoffs dropped. Long-term unemployment also remained unchanged, and labour force participation held at 62.7%.

International – Producer Prices Ease in the Eurozone, Modest Growth in Eurozone Retail Sales, Easing Growth in China’s Services Sector

Eurozone annual inflation fell to 2.2% in August, the lowest since July 2021, primarily due to a sharp drop in energy costs. Despite this, inflation for services and food increased slightly, keeping overall inflation stable.

The Eurozone unemployment rate decreased to a record low of 6.4% in July, with the number of unemployed individuals falling by 114K. Youth unemployment also decreased slightly, with Spain still having the highest unemployment rate among major economies.

Tokyo’s core consumer price index rose by 2.4% in August, the highest in six months, signaling a continued hawkish stance from the Bank of Japan. The headline inflation also increased, surpassing market forecasts.

Japan's retail sales grew by 2.6% year-on-year in July, slower than growth in June and below expectations. Despite the slowdown, retail spending remained positive, with strong sales in non-store retailers and automobiles.

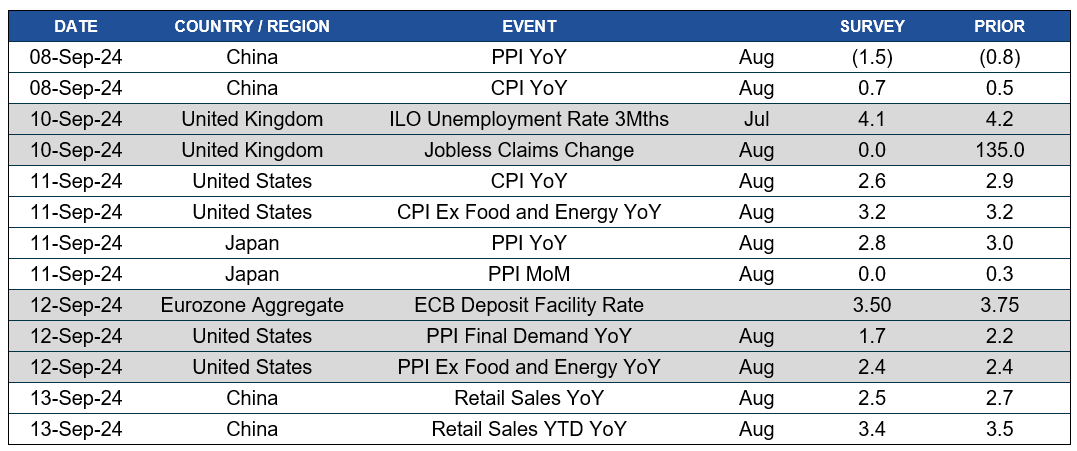

Quick look ahead

As of September 6, 2024